Jun 28, 2023

PART 2. Development of downstream automotive industry

The automotive industry is an important component of the national economy and a key industry for the development of China's manufacturing industry. It has characteristics such as high upstream and downstream correlation, high system integration, high added value, and obvious scale effects. At present, as the largest application market in the die-casting industry, the development of the automotive industry has a huge impact on the development of the die-casting industry.

(1) Overview of the Development of the Automotive Industry

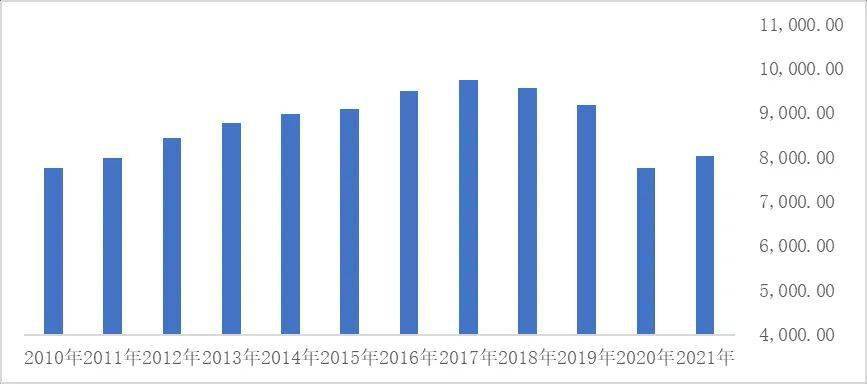

The automobile industry has the characteristics of a long industrial chain. It is tight junction connected with upstream and downstream industries such as steel, nonferrous metals, semiconductor, electronics, energy, logistics, and chemical industry, and can drive the development of a series of fields including tax, employment, and technology. Therefore, the automobile industry has a strong driving role in the industrial upgrading and development of various countries and is also an important symbol of the development level of a country's manufacturing software and hardware strength. According to the data of the World Organization for Automotive Industry (OICA), except that global automobile production declined significantly in 2020 due to the COVID-19, the overall development trend of global automobile production from 2010 to 2019 was good, increasing from 77.6216 million in 2010 to 91.7869 million in 2019. At present, global automobile production is gradually recovering, with a 3.26% increase in 2021 compared to 2020.

Global automobile production from 2010 to 2021 (10000 units)

Data source: OICA

With the rapid development of China's national economy and the rapid progress of manufacturing in recent years, the automotive industry in China has also made significant progress and has become an indispensable and important part of the world's automotive manufacturing industry chain. From the structural components and engines of automobiles to small parts such as accessories and interiors, the figure of Chinese manufacturing can be seen. According to data from CCTV Finance in 2020, the proportion of China's automobile industry to the total GDP is about 6.7%. The automobile industry's driving effect on economic growth is second only to infrastructure and real estate, and has become a strong engine for China's economic development.

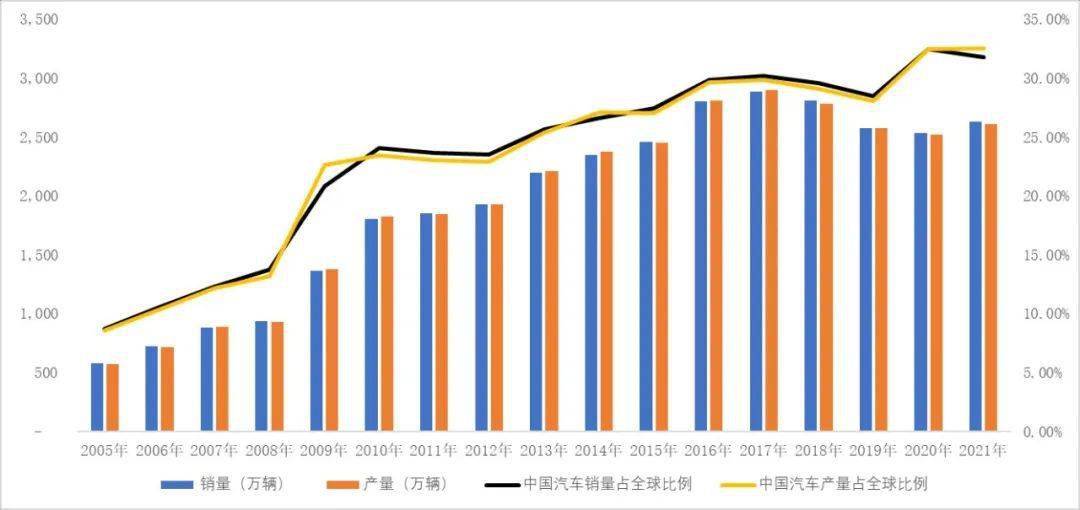

Since entering the new century, China's industrialization, urbanization, and modernization have been rapidly advancing, and the automotive industry in China has begun to maintain a steady upward growth trend. Benefiting from the rapid development of China's economy and various policy support in the automotive industry, China surpassed the United States to become the world's largest automobile producer and seller in 2009 and remained the world's number one. Since 2010, China's automobile production and sales have steadily increased, from 18.26 million units in 2010 and 18.06 million units in sales to 26.08 million units in 2021 and 26.28 million units in sales; The proportion of automobile production and sales to the global market has also steadily increased, from 23.46% in production and 24.06% in sales in 2010 to 32.54% in production and 31.78% in sales in 2021.

China's automobile production and sales situation from 2010 to 2021

Data source: China Association of Automobile Manufacturers

In 2018 and 2019, due to the macro impact of the global automotive market and the comprehensive withdrawal of preferential policies for passenger cars in China, there was a slight decline in the production and sales of automobiles in China. In 2018, China's automobile production and sales decreased by 4.16% and 2.77% compared to the same period last year. In 2019, China's automobile production and sales decreased by 7.51% and 8.23% compared to the same period in 2018. In addition, affected by the COVID-19, China's automobile production and sales continued to decline slightly in 2020, down 1.93% and 1.79% compared with the same period last year. With the end of the domestic epidemic, China's automobile industry is gradually recovering. According to data from the China Association of Automobile Manufacturers, in 2021, China's automobile production was 26.08 million units, an increase of 3.40% year-on-year; China's automobile sales reached 26.28 million units, an increase of 3.81% year-on-year.

Overall, there is still significant room for development in China's automotive market. According to the research report "Embracing the Golden Age of Automobiles - Investment Strategy for the Automotive Industry in 2021" by Dongwu Securities, 90% of China's passenger car sales in 2018 were for first-time purchases and exchanges, with only about 10% of scrapped sales. China's automotive consumption demand is still vast, and the automotive consumption market is far from saturated. In addition, according to data from the Prospective Industry Research Institute, the car ownership per thousand people in China in 2019 was 173 units. Compared to traditional developed and emerging countries, the car ownership per thousand people in China is relatively low, only one-fifth of the car ownership per thousand people in the developed country, the United States. This also indicates that the car consumption market in China has not reached saturation and there is still significant market space to explore.

Comparison of car ownership per thousand people between China and developed and emerging market countries (units)

Data source: Prospective Industry Research Institute

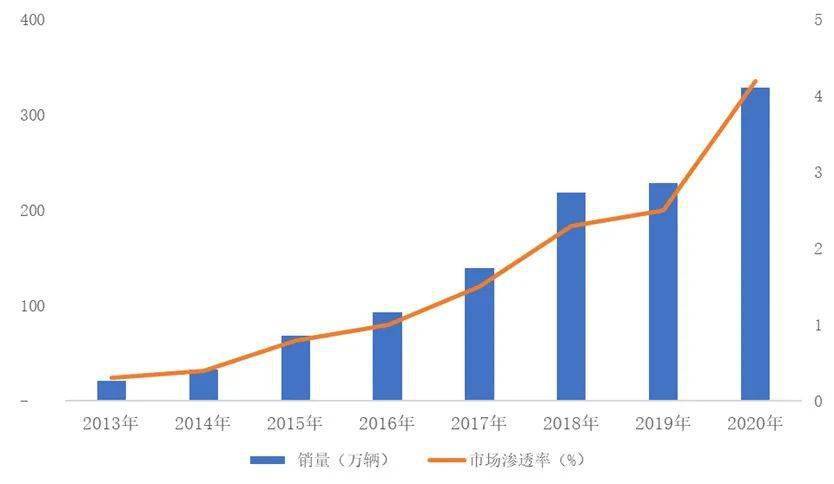

In recent years, the sales of new energy vehicles have grown rapidly. By the end of 2020, new energy vehicles had achieved sales in over 100 countries and regions, with a cumulative global sales of over 11 million vehicles. The compound growth rate of world new energy vehicle sales from 2013 to 2020 reached 47.62%. With countries and regions such as the European Union, China, and the United States gradually increasing their carbon emission regulations, global sales of new energy vehicles have also achieved rapid growth. Compared with 2019, the sales volume of new energy vehicles in 2020 will increase by 1 million, with a growth rate of 43.78%, and the Market penetration will reach 4.2%.

Global sales volume and Market penetration of new energy vehicles from 2013 to 2020

Data source: China Automotive Technology Research Center "China New Energy Vehicle Industry Development Report (2021)"

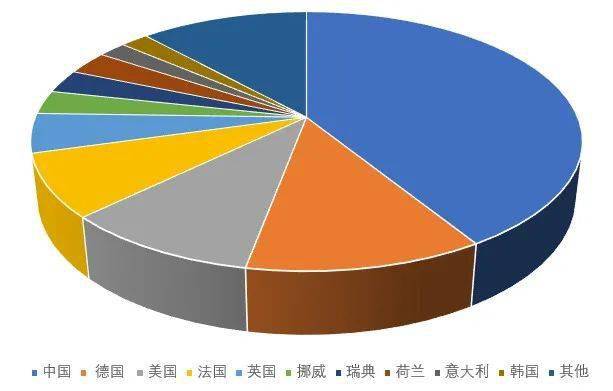

China's new energy vehicles also show a thriving state. Despite the impact of the COVID-19, China's new energy vehicles still achieved a significant positive growth in 2020, with annual sales of 1.367 million vehicles, up 10.9% year on year, accounting for 42% of the world's total sales. The structure of China's new energy vehicle market is gradually optimizing, and the demand for non operational new energy passenger vehicles is gradually increasing. The potential of the new energy vehicle market is gradually becoming prominent. According to data from Dasou Che Zhiyun, in 2021, China sold 2.5646 million non operational new energy passenger vehicles, accounting for 87.8% of the national sales of new energy passenger vehicles, indicating that the main force of new energy passenger vehicles in China has transformed into ordinary consumers, The public's recognition of new energy vehicles is gradually increasing. According to the Technology roadmap 2.0 of Energy Saving and New Energy Vehicles issued by the Chinese Society of Automotive Engineering in October 2020, new energy vehicles will account for about 20% of the total sales by 2025, and 50% of the annual sales of energy saving vehicles and new energy vehicles by 2035. In 2020, the country issued the "New Energy Vehicle Industry Development Plan (2021-2035)", which highlights energy conservation and efficiency enhancement at the policy level, encourages the development of mid to high-end electric vehicles, and points out the direction for the development of new energy vehicles in China. In the future, the new energy vehicle market in China will continue to maintain good development.

Proportion of New Energy Vehicle Sales in Major Global Countries in 2020

Data source: China Automotive Technology Research Center "China New Energy Vehicle Industry Development Report (2021)"

(2) Development of the Automotive Parts Industry

Automotive components refer to various components of a motor vehicle and its body, typically consisting of tens of thousands of components. According to application systems, automotive components can be divided into power systems, transmission systems, suspension systems, steering systems, electrical systems, and other components; According to different materials, automotive components can be divided into metal, plastic, and electronic components. Metal components include traditional iron and steel components, as well as non ferrous metal alloy components such as aluminum, magnesium, and copper.

The automotive parts industry is an important component of the automotive industry and the fundamental support for its development. It promotes and develops together with the automotive industry. In the global automotive industry value chain, the value of the parts industry exceeds 50%. In developed countries, the output value of automotive parts is generally 1.7 times that of the entire vehicle. At present, the automotive industry is characterized by global procurement, and the division of labor and collaboration between major vehicle manufacturers and component manufacturers have formed a pyramid shaped supply structure with vehicle manufacturers at the top and supporting component suppliers at all levels at the bottom. Vehicle manufacturers achieve relative stability in their upstream industrial chain by maintaining their own supplier management system.

According to 360 Research Report statistics, the global automotive parts industry size in 2021 was $1927.79 billion, and it is predicted that the industry size will grow at a compound growth rate of 2.4%, reaching $227375 billion by 2028. At present, the world's automotive parts industry is gradually shifting to emerging countries. Currently, the emerging automotive market is not yet saturated and the market is developing rapidly, making it the main region for vehicle consumption growth. Therefore, it has attracted many international vehicle manufacturers to layout in emerging markets. In addition, emerging markets are located in countries with relatively low labor costs, which has attracted more large automotive component manufacturers to invest and build factories in low labor cost countries, transferring manufacturing links. With the formation of industrial clusters, the costs of automotive component manufacturers will further decrease and gradually attract the transfer of higher technology production links such as research and development, design, procurement, sales, and after-sales, providing a technological foundation for the upgrading of the automotive industry and automotive component industry in these emerging markets.

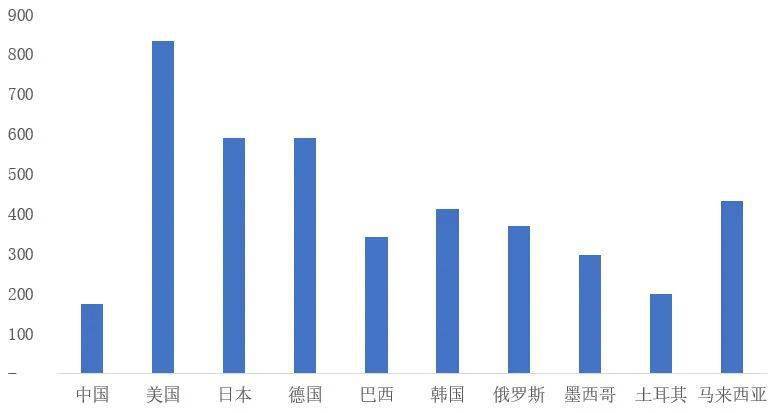

However, currently, the world's automotive parts industry is still dominated by companies from developed countries such as the United States, Japan, Germany, and others that have developed the automotive industry earlier. Currently, these three countries still hold the most seats among the top 100 global automotive companies. According to the annual Global Automotive Parts Top 100 list by AutomotiveNews, there are 23 Japanese companies, 23 American companies, and 18 German companies in the top 100 list, accounting for a total of 64%. A total of 8 automobile parts companies in China have entered the "2021 Global Top 100 Auto Parts List", which is still a certain distance from developed countries that started earlier.

In recent years, the sustained growth of the domestic economy has become an important driving force for the rapid development of the entire vehicle market, thereby promoting the positive development of the automotive parts industry. Against the backdrop of continuous improvement in the industry, domestic component companies continue to increase research and development investment and accelerate industrial upgrading. Multinational automotive component industry giants also attach great importance to the Chinese market, especially in the fields of new energy vehicles and intelligent connected vehicles. They expand their business influence in China by investing in and building factories in China, conducting business with Chinese enterprises, and collaborating on technology. For example, Bosch, BASF, and Continental have invested in China to build factories and expand their business layout in China.

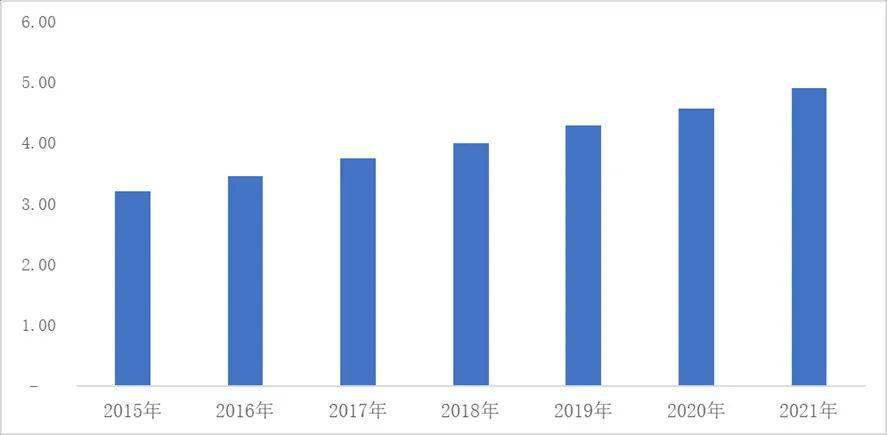

Influenced by macro market factors and the COVID-19, China's auto sales have declined slightly since 2018. However, thanks to the upgrading of China's auto parts industry, the equipment rate of various configurations of auto products has increased significantly, especially the demand for high-value components such as new energy and intelligent networking. China's auto parts industry has maintained a good upward momentum, In 2021, the auto Automotive aftermarket will reach 4.90 trillion yuan. Since 2015, the compound growth rate of the market size in China's automotive parts industry has reached 7.30%.

The scale of China's auto Automotive aftermarket from 2015 to 2021 (trillion yuan)

Data source: China Association of Automobile Manufacturers

The maturity of China's automobile parts enterprises is also reflected in the rapid increase in the export volume of automobile parts in recent years. China's automotive parts industry actively participates in the global layout of the automotive industry chain and has become an important part of the world's automotive parts industry. At present, China has formed six major automobile industry clusters - the Yangtze River Delta industrial cluster, the Southwest industrial cluster, the Pearl River Delta industrial cluster, the Northeast industrial cluster, the Central industrial cluster, and the Bohai Rim industrial cluster. These industrial clusters symbolize that China's automobile industry has matured and have a profound impact on the future development of China's automobile industry.

(3) Development status of aluminum components for automobiles

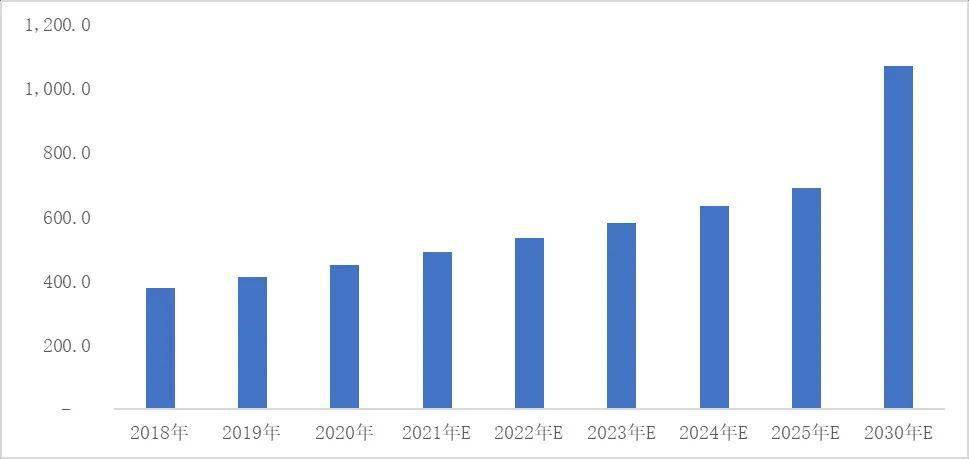

In recent years, the automotive aluminum parts industry has developed rapidly. On the one hand, it has benefited from the continuous demand for lightweight and energy-saving emissions reduction in policies. On the other hand, the demand for the development of the new energy vehicle industry has stimulated the development of the aluminum parts industry on the consumer side. According to the "Assessment Report on Aluminum Consumption in China's Automotive Industry (2016-2030)", the aluminum consumption in China's automotive industry is continuously increasing, reaching 4.506 million tons in 2020. It is expected to reach 10.7 million tons by 2030, with a compound annual growth rate of 8.9%.

Aluminum Consumption in China's Automotive Industry from 2018 to 2030 (10000 tons)

Data source: International Aluminum Industry Association (IAI), CM consulting "Assessment of Aluminum Usage in China's Automotive Industry (2016-2030)" ("Assessment of Aluminum Usage in China's Automotive Industry 2016-2030")

With the increasingly severe environmental problems facing humanity, energy pressure and environmental protection pressure are gradually increasing. Energy conservation, emission reduction, and low carbon have become one of the themes of the current era. China has committed to achieving peak carbon emissions by 2030 and achieving neutrality in carbon emissions by 2060. In the future, China will further attach importance to the role of automobiles in energy conservation, emission reduction, and environmental protection, and strive to achieve greener and more environmentally friendly cars from both new energy vehicles and traditional fuel vehicles. Aiming at the realization method of automobile environmental protection, in the Technology Roadmap of Energy Saving and New Energy Vehicles, the Society of Automotive Engineering of China clearly pointed out that there are three technical paths: the application of lightweight materials, the adoption of new manufacturing technologies and processes, and the adoption of advanced structural optimization or design methods.

Among them, the application of lightweight materials refers to promoting the application of high-strength steel, aluminum alloy, magnesium alloy, engineering plastics, composite materials and other lightweight materials in automotive structures, replacing relatively heavy traditional materials. Aluminum and aluminum alloys, due to their comprehensive performance advantages, have become the best materials for implementing energy-saving and lightweight in automobiles. According to the plan in the Technology Roadmap of Energy Saving and Xinyuan Automobile prepared by the Chinese Society of Automotive Engineering, China's aluminum target for single vehicle is 190 kg in 2020, 250 kg in 2025 and 350 kg in 2030. The demand for aluminum for single vehicle is increasing.

| Advantages of Aluminum and Aluminum Alloys | |

| advantage | Embody |

| Low density |

Aluminum is a common Light metal element with a density of 2.68g/cm3. Compared with the density of steel (7.85g/cm3), the density of aluminum.

Degrees are only one-third of the density of steel, and theoretically, aluminum cars can be reduced by about 30% -40% compared to steel cars, while aluminum engines can be reduced Over 40% weight

|

| Good mechanical strength | Aluminum alloy has excellent impact resistance, and under the same impact strength, aluminum plates are more than ordinary steel plates |

| Absorbs 50% of the impact energy; in terms of strength, aluminum alloy has a specific strength close to that of alloy steel, surpassing that of ordinary steel, thus ensuring zero. Under the overall strength of the components, aluminum alloy components can be made lighter and thinner; Less affected by environmental temperature, aluminum alloy in low-temperature environments. Gold can still maintain good strength and mechanical properties. | |

| Large storage capacity |

Aluminum accounts for 7.4% of the mass fraction in the Earth's crust, making it the most abundant metallic element on Earth, surpassing the most commonly used iron and capable of long-term use.

|

| Environmentally friendly and recyclable |

Aluminum has good recyclability, and the recycling rate of aluminum can reach 90% after recycling, and it needs to be consumed during recycling the energy is only 5% of the initial smelting, demonstrating excellent recyclability.

|

| Good thermal conductivity | The thermal conductivity of aluminum is 237w/m · K, second only to precious metal silver and non-ferrous metal copper, ranking third and several times higher than ordinary carbon steel. Compared to copper and silver, although aluminum has lower thermal conductivity, its cost is much lower. In addition; Aluminum has a much lower density than copper and silver, and can effectively reduce the weight of the vehicle body when used as a component metal for heat dissipation fins. It is an excellent material for automotive heat dissipation fins. |

| Excellent ductility performance | Aluminum has excellent ductility, ranking third only to gold and silver in terms of ductility. Aluminum can be stretched into thin films thinner than 0.01mm under conditions of 100 ℃ -150 ℃. 1g of aluminum can pull out 37m of fine wires, making it easy to process and has strong processing performance. |

| Good corrosion resistance | During the use of a car, it will face various working conditions, such as rain, excessive water, and exposure to sunlight. Aluminum has good corrosion resistance and only corrodes in concentrated acids and alkalis. Aluminum automotive components can be used for long-term service with their excellent corrosion resistance. |

Source: Huajin Securities, "Aluminum: Synergy between Supply and Demand, Beyond the Cycle"

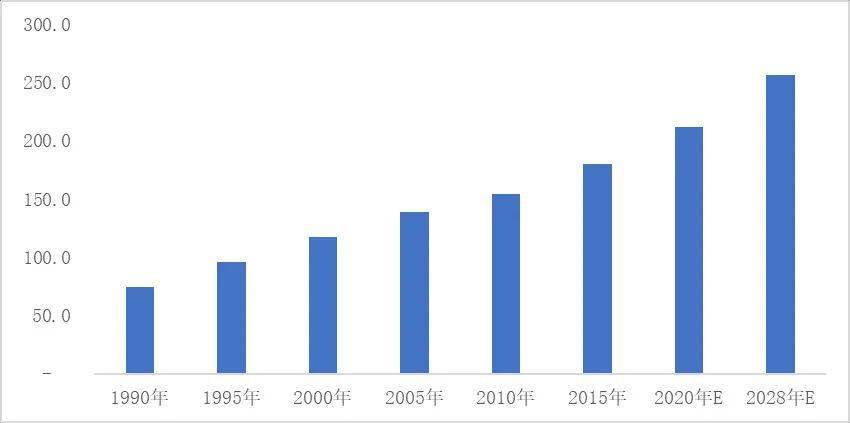

From a market perspective, replacing steel with aluminum in automobiles has become a global trend in the lightweight development of automobiles. Taking the North American market, which has been developing for a long time and is relatively mature, as an example, according to research by Ducker Worldwide, from 1990 to 2020, the aluminum consumption per light vehicle in North America is expected to increase from 74.8kg to 211.37kg, with a growth rate of 182.58%. It is predicted that the aluminum content of light vehicles will further increase in the future, reaching 256.28 kg by 2028.

Changes in Aluminum Consumption per Light Vehicle in North America (kg)

Data source: DuckerWorldwide

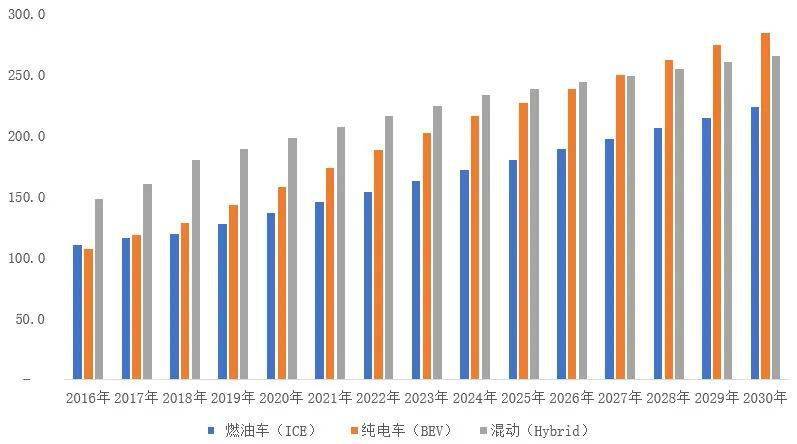

With the maturity and development of China's automotive industry, the amount of aluminum used by individual cars in China is also gradually increasing. According to research reports from the International Aluminum Industry Association and CM Consulting, the amount of aluminum used by individual cars in passenger cars in China has been continuously increasing since 2016, and the research report predicts that the amount of aluminum used by passenger cars in China will further increase in the future.

Changes and Forecast of Aluminum Consumption per Vehicle in China's Automotive and Passenger Cars from 2016 to 2030 (kg)

Ningbo Fuerd was founded in 1987 and is a leading full-service die Casting Tooling, aluminum die casting, zinc die casting, and Gravity casting manufacturer. We are a solution provider offering a wide array of capabilities and services that include engineering support, designing, molds, complex CNC machining, impregnation, tumbling, chrome, powder coating, polishing, assembly, and other finishing services. We will work with you as partners, not just suppliers.